Common Home Insurance Mistakes: Are You Making These Costly Errors?

Home insurance is a crucial safeguard for homeowners, yet many still make common home insurance mistakes that can lead to significant financial losses. One of the most prevalent errors is underinsurance, where homeowners fail to assess the full replacement cost of their property. This can result in insufficient coverage during a claim, leaving them with unexpected out-of-pocket expenses. Additionally, neglecting to review and update policy details regularly can lead to lapses in coverage when major renovations or purchases are made. Always ensure your coverage aligns with the current value of your home and its contents.

Another frequent mistake is not shopping around for the best rates. Many homeowners stick with their current insurance provider without comparing policies, potentially missing out on better coverage options or lower premiums. According to experts, it's advisable to review your home insurance policy at least once a year. Common home insurance mistakes can also include assuming that all personal belongings are covered under a standard policy. Items of value, like jewelry or art, often require additional coverage. To avoid these costly errors, make it a habit to evaluate your policy and discuss your coverage needs with an insurance agent.

What Does Your Home Insurance Really Cover? Top 5 Surprising Exclusions

When you purchase home insurance, you might believe that your policy covers almost anything that could happen to your home. However, many homeowners are surprised to discover that certain incidents and items are often excluded. In this article, we will explore the top five surprising exclusions that can leave you vulnerable and unprotected.

- Flood Damage: One of the most common exclusions in home insurance policies is damage caused by flooding. Standard policies typically do not cover water damage from heavy rains or overflowing bodies of water. Homeowners in flood-prone areas may need to consider separate flood insurance to properly protect their assets.

- Earthquakes: Similar to flooding, earthquakes are often not covered under standard home policies. If you live in an area prone to seismic activity, you might want to look into earthquake insurance to safeguard against this natural disaster.

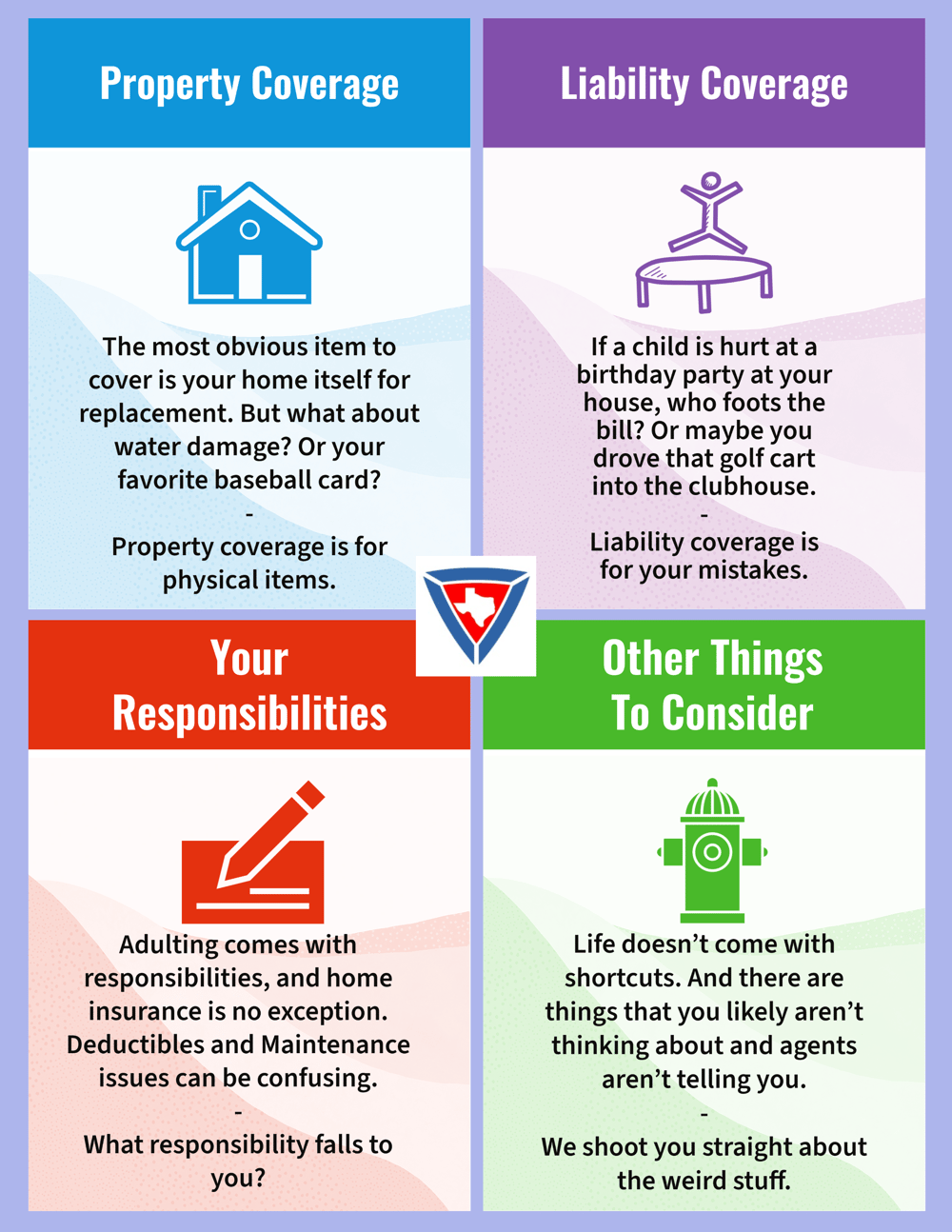

- Wear and Tear: Home insurance policies aim to cover unexpected damage, but they typically do not cover wear and tear from normal usage. Maintenance issues such as a leaky roof or aging appliances often fall under the responsibility of the homeowner.

- Pest Infestations: Many policies exclude damage caused by pests like termites or rodents. Homeowners must be vigilant about maintaining their property to avoid these pests, as insurance won't cover the resulting damage.

- High-Value Items: Items such as jewelry, art, and collectibles often have limited coverage on standard home insurance policies. If you own valuable items, it’s essential to assess your coverage and consider an endorsement or separate policy to protect them adequately.

Is Your Home Insurance Policy Ready for Natural Disasters?

As extreme weather events become increasingly common, it's vital to assess whether your home insurance policy is equipped to handle the financial fallout from natural disasters. Many homeowners assume that their standard policy will sufficiently cover damage from incidents like floods, earthquakes, or wildfires; however, this is often not the case. Review your policy to determine what types of natural disasters are included in your coverage and whether additional riders are necessary to protect your home and belongings.

Furthermore, understanding your local risks can significantly impact your coverage needs. Areas prone to specific natural disasters, such as hurricanes or tornadoes, may require specialized insurance. Consider consulting with an insurance professional to tailor your home insurance policy according to the risks prevalent in your region. By taking these proactive steps, you ensure that your home is prepared for nature's unpredictability, ultimately safeguarding your family's financial future.